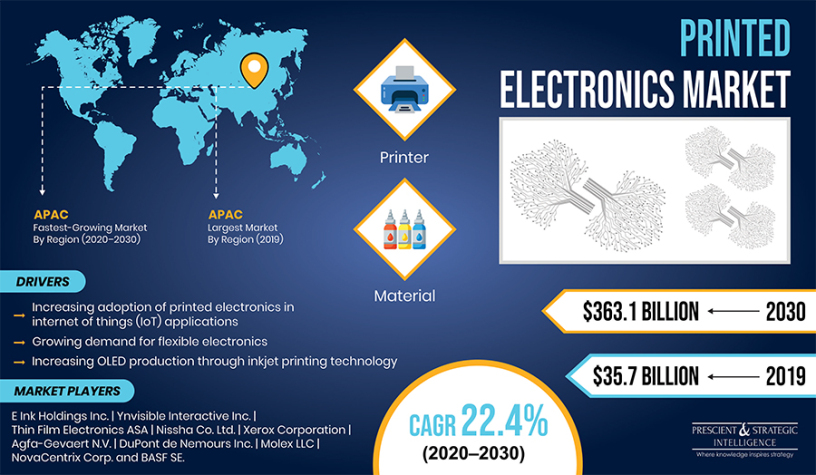

From $35.7 billion in 2019, the global printed electronics market revenue is expected to surge to $363.1 billion by 2030. According to the estimates of the market research company, P&S Intelligence, the market will advance at a CAGR of 22.4% from 2020 to 2030 (forecast period). The growing adoption of printed electronics in internet of things (IoT) applications, mushrooming need for flexible electronics, and soaring OLED production with the help of the inkjet printing technology are the major factors propelling the advancement of the market across the globe.

The growing requirement for flexible electronics is a major printed electronics market growth driver. In these products, integrated circuits (ICs) are incorporated on a flexible substrate, such as a metal or a plastic, which can be easily rolled, wrapped, twisted, or folded, without hampering the function. Because of the rising demand for these substances, the players operating in the industry are announcing collaborations with technology providers. For instance, E Ink Holdings Inc. announced a collaboration with Plastic Logic HK in June 2019 for using the organic field-effect transistor (OTFT) technology for producing flexible electronic paper displays for wearables.

Browse detailed – Printed Electronics Market Revenue Estimation and Growth Forecast Report

Depending on component, the printed electronics market is divided into material and printer categories. Of these, the material category is predicted to exhibit faster growth in the upcoming years. This is ascribed to the soaring adoption of inks and substrates in the fabrication of printed electronic circuits, which are then used in several applications, such as RFID tags, PVs, and displays. For example, researchers working in the U.S. Army Combat Capabilities Development Command’s (CCDC) chemical-biological centers completed the successful testing of a light-emitting diode (LED) light on clothing in 2019.

When end user is taken into consideration, the market is categorized into automotive and transportation, healthcare, consumer electronics, aerospace and defense, retail and packaging, and construction and architecture. Out of these, the automotive and transportation category held the largest share in the market in the past. This was because of the large-scale utilization of the IoT technology in the automotive and transportation sector. The adoption of IoT requires a high bandwidth and extensive data processing capabilities for supporting the remote sensing technology and multiple connections in collecting data from connected devices.

Printed Electronics Market Value To Surpass $350.0 Billion by 2030

Globally, the Asia-Pacific (APAC) region is predicted to be the fastest-growing region in the printed electronics market during the forecast period. The market in the region is being propelled by the rising requirement for consumer electronics in nations, such as India, China, South Korea, Australia, and Japan. As the printed electronics technology is being increasingly incorporated in the production of flexible consumer electronics, such as wearable devices, the soaring use of these electronics is predicted to fuel the growth of the market in the region in the coming years.

Thus, the demand for printed electronics will shoot up in the forthcoming years, mainly because of its increasing deployment in IoT applications and the burgeoning requirement for flexible electronics across the world.

Factors such as the burgeoning demand for flexible electronics and increasing organic light-emitting diode (OLED) production through inkjet printing technology will drive the printed electronics market at a CAGR of 22.4% during the forecast period (2020–2030). According to P&S Intelligence, the market was valued at $35.7 billion in 2019 and it is projected to generate $363.1 billion revenue by 2030. In recent years, the increasing shift from conventional to digital printing has become a key market trend.

How Is High Flexible Electronics Demand Boosting Printed Electronics Market Growth?

The accelerating demand for flexible electronics is a prominent growth driver for the market across the world. Integrated circuits (ICs) are deployed on flexible substrates, such as metal or plastic, of electronics to convert them into flexible electronics. The integration of ICs on flexible substrates does not impact the function of such electronics. For instance, in June 2019, E Ink Holdings Inc. collaborated with Plastic Logic HK to use organic field-effect transistor (OTFT) technology for producing flexible electronic paper displays for wearables.

Nowadays, the surging preference for digital printing over conventional printing, primarily on account of the growing environmental concerns, has become a prominent trend in the printed electronics market. Conventional printing involves the usage of volatile organic compound (VOC)-based products, such as chromium, lead, mercury, cadmium, paint strippers, and aerosol sprays, which massively contribute to the escalating water and soil pollution levels. Whereas, digital printing is highly eco-friendly, as it includes the use of less harmful chemicals and mild solvents, as compared to the ones used in conventional printing technologies, such as solid ink printing and offset printing.

Printed Electronics Market Revenue Estimation and Growth Forecast Report

At present, the printed electronics market is extensively competitive, due to the presence of a large number of regional and global players worldwide. The leading players in the market, such as Ynvisible Interactive Inc., E Ink Holdings Inc., Thin Film Electronics ASA, NovaCentrix Corp., Agfa-Gevaert N.V., Nissha Co. Ltd., BASF SE, Xerox Corporation, and DuPont de Nemours Inc. are currently focusing on partnerships and mergers and acquisitions to expand their geographical presence.

The component segment of the printed electronics market is bifurcated into printer and material. Of these, the printer category generated the higher revenue in 2019, due to the mushrooming demand for inkjet and screen printers for photovoltaic (PV) and display applications in countries such as China, Germany, Brazil, the U.A.E., and the U.S. Whereas, the material category is expected to demonstrate the faster growth during the forecast period, due to the increasing use of inks and substrates in the fabrication of printed electronic circuits, which are being increasingly used in PV cells, displays, and RFID tags.

Recent Strategic Developments of Major Printed Electronics Market Players

Geographically, Asia-Pacific (APAC) accounted for the largest share in the printed electronics market in 2019, and it is also expected to witness the fastest growth throughout the forecast period. This is attributed to the burgeoning demand for robust and flexible substrates for printed electronic circuits and rising penetration of the internet of things (IoT) technology in the region. Additionally, the low manufacturing cost and continuous developments in digital printing technology will also facilitate the market growth in the region in the coming years.

Therefore, the mounting demand for flexible electronics and rising preference for digital printing will augment the market growth in the forthcoming years.

Chapter 1. Research Background

1.1 Research Objectives

1.2 Market Definition

1.3 Research Scope

1.3.1 Market Segmentation by Component

1.3.2 Market Segmentation by Application

1.3.3 Market Segmentation by End-User

1.3.4 Market Segmentation by Region

1.3.5 Analysis Period

1.3.6 Market Data Reporting Unit

1.3.6.1 Value

1.4 Key Stakeholders

Chapter 2. Research Methodology

2.1 Secondary Research

2.2 Primary Research

2.2.1 Breakdown of Primary Research Respondents

2.2.1.1 By region

2.2.1.2 By industry participant

2.2.1.3 By company type

2.3 Market Size Estimation

2.3.1 By Value

2.4 Data Triangulation

2.5 Assumptions for the Study

Chapter 3. Executive Summary

Chapter 4. Introduction

4.1 Definition of Market Segments

4.1.1 By Component

4.1.1.1 Printer

4.1.1.1.1 Screen

4.1.1.1.1.1 Rotary

4.1.1.1.1.2 Flatbed

4.1.1.1.2 Inkjet

4.1.1.1.2.1 Continuous

4.1.1.1.2.2 Drop-on-Demand

4.1.1.1.3 Offset

4.1.1.1.4 Flexographic

4.1.1.1.5 Gravure

4.1.1.1.6 Others

4.1.1.2 Material

4.1.1.2.1 Substrates

4.1.1.2.1.1 Inorganic

4.1.1.2.1.2 Organic

4.1.1.2.2 Inks

4.1.1.2.2.1 Conductive

4.1.1.2.2.2 Dielectric

4.1.2 By Application

4.1.2.1 Display

4.1.2.1.1 Electroluminescent

4.1.2.1.2 Electronic paper (E-Paper)

4.1.2.2 PV

4.1.2.3 Lighting

4.1.2.4 Sensors

4.1.2.5 RFID tags

4.1.2.6 Batteries

4.1.2.7 Others

4.1.3 By End-User

4.1.3.1 Automotive & transportation

4.1.3.2 Consumer electronics

4.1.3.3 Healthcare

4.1.3.4 Retail & packaging

4.1.3.5 Aerospace & defense

4.1.3.6 Construction & architecture

4.1.3.7 Others

4.2 Value Chain Analysis

4.3 Market Dynamics

4.3.1 Trends

4.3.1.1 Shift from conventional to digital printing

4.3.1.2 Miniaturization of devices

4.3.2 Drivers

4.3.2.1 Increasing adoption of printed electronics in internet of things (IoT) applications

4.3.2.2 Growing demand for flexible electronics

4.3.2.3 Increasing OLED production through inkjet printing technology

4.3.2.4 Impact analysis of drivers on the market forecast

4.3.3 Restraints

4.3.3.1 Established market for rigid electronic products

4.3.3.2 Impact analysis of restraints on the market forecast

4.3.4 Opportunities

4.3.4.1 Inclination toward online reading materials

4.3.4.2 Building electronics using additive manufacturing

4.4 Porter’s Five Forces Analysis

Chapter 5. Global Market Size and Forecast

5.1 By Component

5.1.1 By Printer Type

5.1.1.1 By inkjet type

5.1.1.2 By screen type

5.1.2 By Material

5.1.2.1 By substrates type

5.1.2.2 By inks type

5.2 By Application

5.2.1 By Display Type

5.3 By End-User

5.4 By Region

Chapter 6. North America Market Size and Forecast

6.1 By Component

6.1.1 By Printer Type

6.1.1.1 By inkjet type

6.1.1.2 By screen type

6.1.2 By Material

6.1.2.1 By substrates type

6.1.2.2 By inks type

6.2 By Application

6.2.1 By Display Type

6.3 By End-User

6.4 By Country

Chapter 7. Europe Market Size and Forecast

7.1 By Component

7.1.1 By Printer Type

7.1.1.1 By inkjet type

7.1.1.2 By screen type

7.1.2 By Material

7.1.2.1 By substrates type

7.1.2.2 By inks type

7.2 By Application

7.2.1 By Display Type

7.3 By End-User

7.4 By Country

Chapter 8. APAC Market Size and Forecast

8.1 By Component

8.1.1 By Printer Type

8.1.1.1 By inkjet type

8.1.1.2 By screen type

8.1.2 By Material

8.1.2.1 By substrates type

8.1.2.2 By inks type

8.2 By Application

8.2.1 By Display Type

8.3 By End-User

8.4 By Country

Chapter 9. LATAM Market Size and Forecast

9.1 By Component

9.1.1 By Printer Type

9.1.1.1 By inkjet type

9.1.1.2 By screen type

9.1.2 By Material

9.1.2.1 By substrates type

9.1.2.2 By inks type

9.2 By Application

9.2.1 By Display Type

9.3 By End-User

9.4 By Country

Chapter 10. MEA Market Size and Forecast

10.1 By Component

10.1.1 By Printer Type

10.1.1.1 By inkjet type

10.1.1.2 By screen type

10.1.2 By Material

10.1.2.1 By substrates type

10.1.2.2 By inks type

10.2 By Application

10.2.1 By Display Type

10.3 By End-User

10.4 By Country

Chapter 11. Competitive Landscape

11.1 List of Key Players and Their Offerings

11.2 Analysis of Key Players in the Market

11.3 Competitive Benchmarking of Key Players

11.4 Recent Activities of Key Market Players

11.5 Strategic Developments of Key Players

11.5.1 Mergers & Acquisitions

11.5.2 Product Launches

11.5.3 Partnerships

11.5.4 Other Developments

Chapter 12. Company Profiles

12.1 Agfa-Gevaert N.V.

12.1.1 Business Overview

12.1.2 Product and Service Offerings

12.1.3 Key Financial Summary

12.2 Thin Film Electronics ASA

12.2.1 Business Overview

12.2.2 Product and Service Offerings

12.2.3 Key Financial Summary

12.3 Nissha Co. Ltd.

12.3.1 Business Overview

12.3.2 Product and Service Offerings

12.3.3 Key Financial Summary

12.4 Ynvisible Interactive Inc.

12.4.1 Business Overview

12.4.2 Product and Service Offerings

12.5 Xerox Corporation

12.5.1 Business Overview

12.5.2 Product and Service Offerings

12.5.3 Key Financial Summary

12.6 DuPont de Nemours Inc.

12.6.1 Business Overview

12.6.2 Product and Service Offerings

12.7 Molex LLC

12.7.1 Business Overview

12.7.2 Product and Service Offerings

12.8 NovaCentrix Corp.

12.8.1 Business Overview

12.8.2 Product and Service Offerings

12.9 BASF SE

12.9.1 Business Overview

12.9.2 Product and Service Offerings

12.9.3 Key Financial Summary

12.10 E Ink Holdings Inc

12.10.1 Business Overview

12.10.2 Product and Service Offerings

12.10.3 Key Financial Summary

Chapter 13. Appendix

13.1 Abbreviations

13.2 Sources and References

13.3 Related Reports

Add Comment